Notwithstanding the federal shutdown and impasse, the much ballyhoo'ed launch of the PPACA Health Insurance Exchanges went off as scheduled on October 1st while we were at Health 2.0 2013 in Santa Clara.

I spent a bit of time last night surfing around the "Covered California" HIX website.

There will be a lot of unhappy "young invincibles," young, health adults who continue to think they don't need health insurance. After visiting these HIX sites, they will likely not be pleased at what they find -- a lot of "sticker shock" (policy pricetags) and "benefits shock" (out-of-pocket stuff: exclusions, deductibles, and co-pays). Those of us who don't get health insurance through our employers are henceforth to be Individually Mandated Bronze, Silver, Gold, or Platinum people.

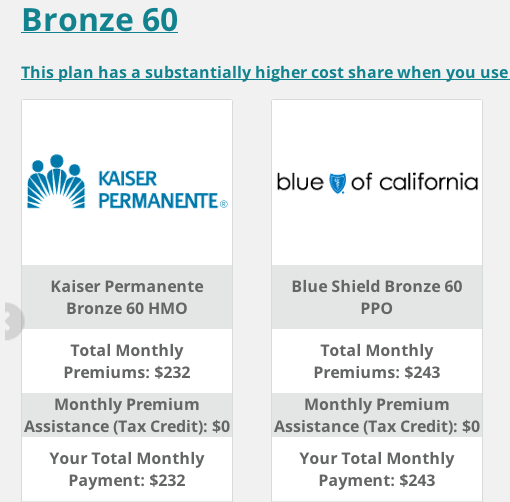

Let's look at some Bronze and Silver scenarios for a 30 year old single male earning $40k a year.

Look just at the cheapest Bronze (the Kaiser HMO plan). This fellow will have to fork over $2,784 a year just for the policy (sticker shock), and will then be on the hook for virtually all routine medical expenses up to the out-of-pocket cap (benefits shock -- or, more precisely, "lack-of-benefits shock").

The only year-over year-benefit here is the actual "insurance" piece -- i.e., the "catastrophic" coverage part. The rest is not "insurance," it's "pre-payment" for services that may not be needed for years (in after-tax dollars, I might add). Also, say our $40k earner really only takes home $32k after all deductions. The $6,350 out-of-pocket cap would be ~20% of take-home. Reasonable?

It should be noted that if this hypothetical young man is only making, say, $20k per year, federal subsidies would apply to offset these retail policy prices.

In the foregoing example, assuming no UTIL over the year, the $2,784 (subsidy offsets or not) is essentially a de facto "tax," one not paid into the U.S. Treasury but paid to private health insurance companies.

If the Young Invincibles refuse en masse to jump into the ObamaCare risk pool, the PPACA will simply not work. You're asking young workers to purchase an expensive abstraction. You can touch and feel and watch a top-of-the-line 72" plasma HDTV. You can ride on a nice motorcycle, or ride in a nice power boat. You can take a pretty nice foreign vacation for three grand. A health care "policy," something that you don't want to have to use (and won't if you remain healthy), is quite another matter psychologically.

And then, from THCB's "How I Learned to Stop Worrying and Love Obamacare” comes this bit of AM radio-esqe comic relief pushback in the comments:

Jardinero1 says:Add some Xanax to your EHR Active Meds List, pal.

I accept your feelings about the ACA, Ted Cruz and the ACA but the exchanges are not “the most pro-market thing to emerge from this administration.” They do not fit the definition of markets.

Markets are where willing sellers and willing buyers meet without coercion. In the absence of coercion, willing sellers and willing buyers agree on the quality of the good and the price or they agree to walk away from one another.

The ACA’s health Insurance exchanges have none of those features. Health insurance exchanges are a state created medium where coerced buyers are forced to buy a product assembled via government edict from a cartel of sellers established by government edict. You could be partially correct if you assert that the state mandated exchange have elements of fascism, state capitalism, or crony capitalism. But call it market based and you are almost wholly incorrect.

By coercion, I refer to the threat of violence, loss of freedom (incarceration), or involuntary loss of property (extortion, taxes, fines) under pain of violence or the loss of freedom. Coercion is unique to state mandated activities and organized crime. Free markets are about willing buyers and willing sellers. Forcing people into a room and telling them they have to deal or face the coercion I describe is not a market and not even a market principle.

Monday morning update. apropos of the foregoing, from the NEP Behind the Crisis in American Governance: Delusions about the Economy Treated As a Matter of Differing Economic “Taste”:

...Ultimately the fantasy-laden vision that has developed is that capitalism as represented by loosely regulated or unregulated markets is an autonomous, self-stabilizing system that at the same time paradoxically is fragile and mercurial enough to require political and economic “courtship” and “soothing” by local, regional and national governments. Furthermore, this system of economic beliefs suggests that market institutions could do the job of government better than government itself, so it always makes sense for policymakers to try to create markets where there are now government institutions. The fantasy presented is that government is an entirely fallible institution and markets are a nearly infallible institution. If this delusion is assumed as a given, as has been hammered into people’s brains for three decades, logically it makes sense to pare government as much as possible and allow the private sector to attempt to take over its functions..."Interesting" times ahead. Anxious times ahead.

UPDATE: OCT 8th TUESDAY MORNING SF GATE HEADLINE

Obama sold voters bill of goods on health care

Debra J. Saunders

As a candidate for president, Barack Obama sold his signature universal health care plan with the promise that it would "cut the cost of a typical family's premium by up to $2,500 a year."Whether these anecdotes comprise a significant empirical trend or not, it doesn't take more than a relative handful of such stories to turn people off.

Now that the Affordable Care Act exchanges are open for business, voters are finding that the biggest problem with Obamacare isn't that some Web sites crashed last week but that the Obama promise of big savings for the average family was too good to be true.

Now that the exchanges are open for business, people who already have individual coverage have something new to not like: sticker shock. The Affordable Care Act isn't affordable after all.

Last week, I began hearing from readers whose individual policy premiums are going up, not down. A local architect sent me a notice he received from Kaiser informing him that his individual coverage will increase by $199.95 per month, or 78.9 percent. When he added his two sons, the percentage increase was even greater.

A freelance journalist told me she made $98,000 last year. But she and her retired husband, both 51, wouldn't pay $7,200 in premiums for high-deductible coverage. It's cheaper to pay the fine, she said. Besides, she added, "we're healthy."...

__

None of any of the foregoing has anything directly to do with Health IT, of course, but these various pieces of the U.S. health care "system" are increasingly intertwined. Broad support for the PPACA was palpable at Health 2.0 this past week. There's a lot riding on its success.

SNL GOES OFF THE HOOK ON THE SHUTDOWN

Lordy...

The proactive Miley Cyrus parodied her viral song "We Can't Stop" and mocked the U.S. government shutdown on Saturday Night Live. In the pre-taped music video titled "We Did Stop (The Government)," the 20-year-old pop star played congresswoman Michele Bachmann as funny man Taran Killam assumed the role of House Speaker John Boehner.

"It’s our party, we can stop what we want, we can vote how we want, defund what we want," Cyrus sings. "Red states and sweaty bodies everywhere, bill’s in the house like we don’t care, 'cause we came to shut it all down now, no government around now. If you’re not ready for health care, can I get a “hell no!” 'Cause we’re gonna keep it out shut down, D.C.is a closed town all around."

BELOW: SAVE THE DATE

Twitter hashtag #ingniteinterop. Website here.

MONDAY MORNING UPDATE

Dangerous game of Chicken going on.

BACK to Health IT

"...Clearly, the usability of EHRs has gotten worse with the implementation of Meaningful Use. Many have been coded to certification requirements, not designed to make achieving Meaningful Use a byproduct of improved workflow automation. Where basic EHR usage is not already established, bolted on functionality forces clinicians to take additional steps that further disrupt workflow..."From Darwinian health IT: Only well-designed EHRs will survive.

I'm havin' a Clinic Monkey Moment.

TUESDAY UPDATE

Went to an ASQ Section 618 meeting last night in Oakland. Met a lot of very nice people. I'll be switching my Section membership from Las Vegas 705 to the East Bay Section forthwith. I have to get back into being more active in the Society.

|

| www.asqeastbay.org |

Great banner photo.

More HIX chatter from HealthCare IT News.

Doctors cautious about HIX, says MGMAPPACA IN ONE MARKED UP GRAPH

40 percent of responding physician practices say they're still weighing their options

Diana Manos, October 7, 2013

...A week into the open enrollment period for ACA insurance exchanges, 40 percent of responding physician practices reported that they are still weighing their options as to whether or not they will participate with new exchange insurance products...

"Medical group practices want to continue to do the right thing and take care of patients, regardless of insurance. It’s troublesome that there is so much uncertainty about ACA implementation this late in the game," said Susan L. Turney, MD, MGMA president and CEO in a news release. "Some insurers want practices to sign contracts for less than their current commercial rates, but are unable or unwilling to provide detailed information to physicians about how the exchange products will be administered."...

I did a quick Photoshop on the above. On average, health care utilization is a function of aging. We know this, and have known it for a long time. "ObamaCare" is nothing more than a broad redistributional flattening (orange line) of the heretofore prevalent health insurance underwriting model (the red line). The actual "actuarial risk envelope" is 60-70 (adult) years, not one. Once you advance to middle age, you've started costing the insurors money, which they have historically tried to make up by raising rates on the aging, or finding reasons ("pre-existing conditions") to exclude them.

So, yes, the "young have to subsidize the old" in any rational system. But those young will themselves advance to old age, to be reciprocally "subsidized" by the young who follow them. Absent such a payment scheme, the old (with the exception of the very wealthy) will be priced out. No insuror wants to underwrite Grandma.

That's pretty much all there is comprising the topic of this huge political fight now at the center of the acrimonious, paralyzing federal shutdown and looming risk of debt default.

Yes, there are QI pilots contained in the PPACA intended to "bend the UTIL cost curve" down, and advances in medtech such as I just witnessed at Health 2.0 2013 may well abate some costs materially. But, "ObamaCare" is really just insurance reform -- reform that the AHIP members themselves bought into.

CODA

Reposting my ObamaCare song, penned in the wake of the SCOTUS ruling last year.

___

More to come...

No comments:

Post a Comment